The #1 Reason Buyers Walk Away (And How To Get Ahead of It)

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

The Top Dealbreaker: Issues That Pop Up During the Inspection

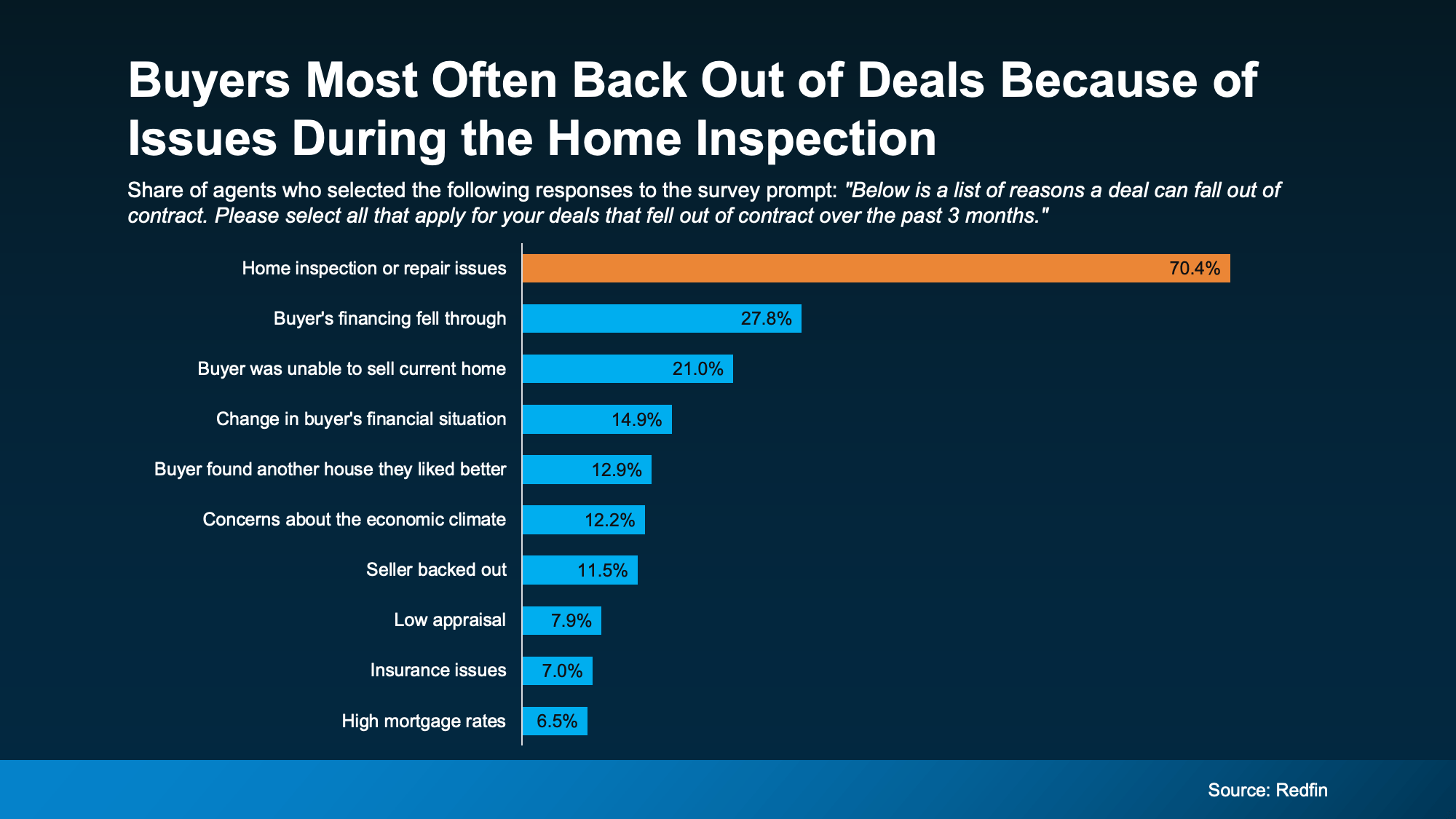

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

Why Fixing Things Before You List Matters More Today

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

How Your Agent Can Help Give You the Edge

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They’ll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

- Roof leaks or damage: sagging, leaking, etc.

- Plumbing problems: standing water, leaks, water damage, etc.

- Electrical concerns: outdated or exposed wiring, missing GFCI outlets, etc.

- HVAC issues: non-functioning units

- Pest or insect damage: termite colonies, etc.

- Hazardous materials: lead, mold, asbestos, etc.

- Safety/code violations: missing smoke detectors, windows stuck closed, etc.

- Structural problems: cracks in the foundation, sagging floors, etc.

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

The Benefits of a Pre-Listing Inspection

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

- Fix concerns before you list, or disclose issues upfront

- Avoid having to respond or negotiate under pressure

- Stop scrambling to find contractors with availability before your closing date

But remember, you don’t have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

- Decide if a pre-listing inspection is worth it where you live

- Recommend a trusted inspector (if you decide to get one)

- Look at the results with you to identify true dealbreakers in your market

- Help you decide what to fix or what to credit

- Make sure you avoid over-spending or under-preparing

Bottom Line

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, connect with an agent.

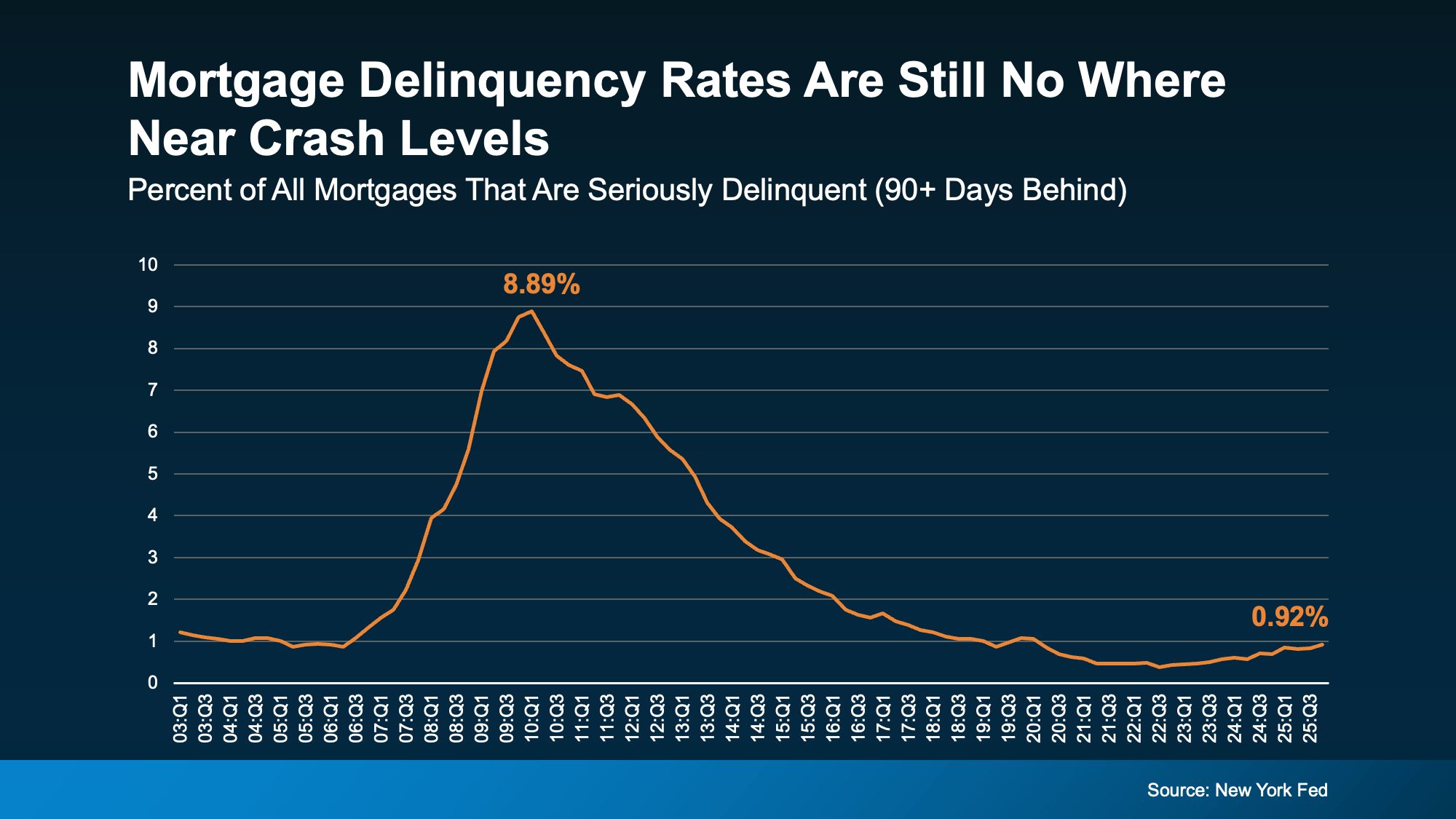

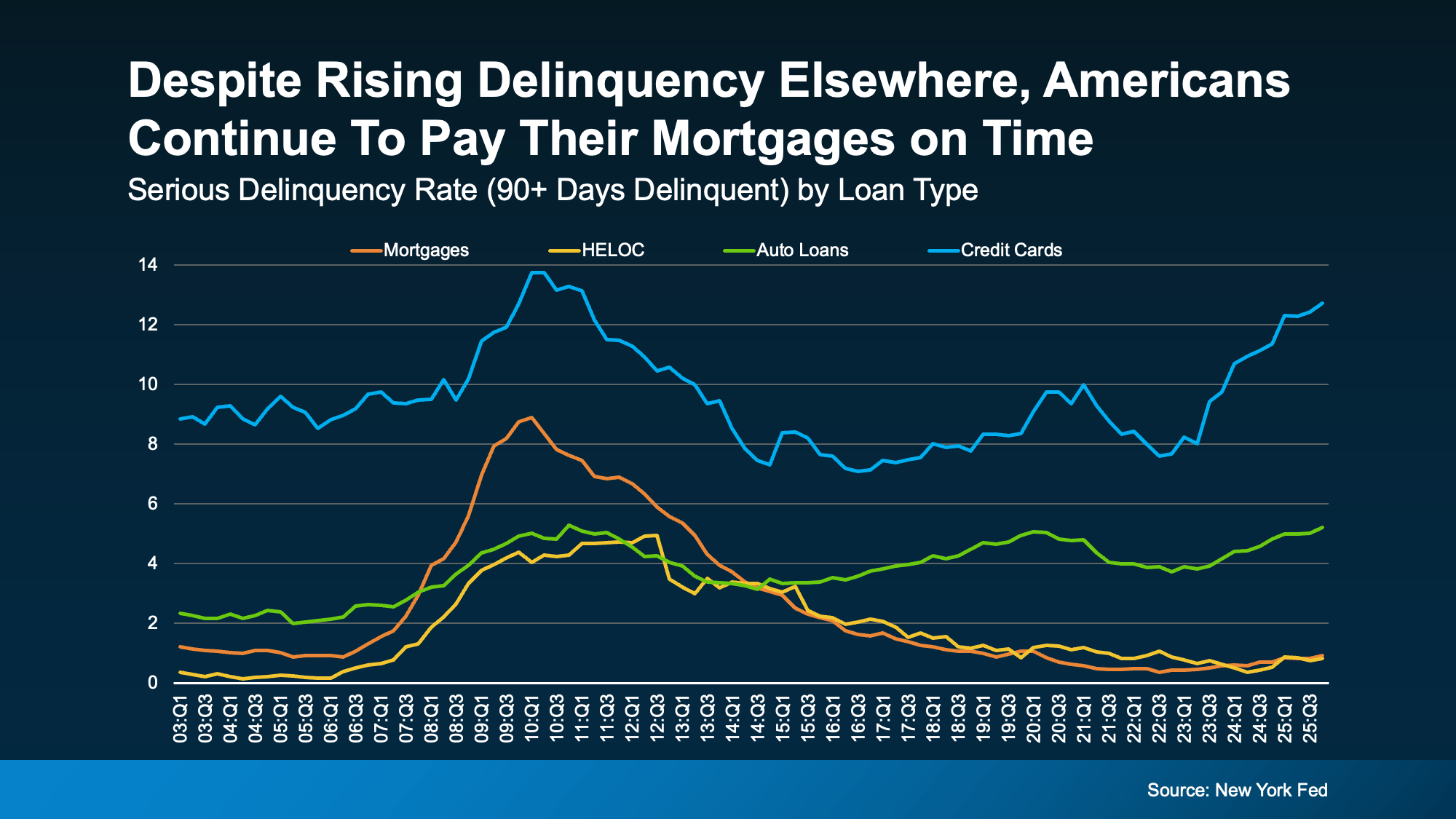

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

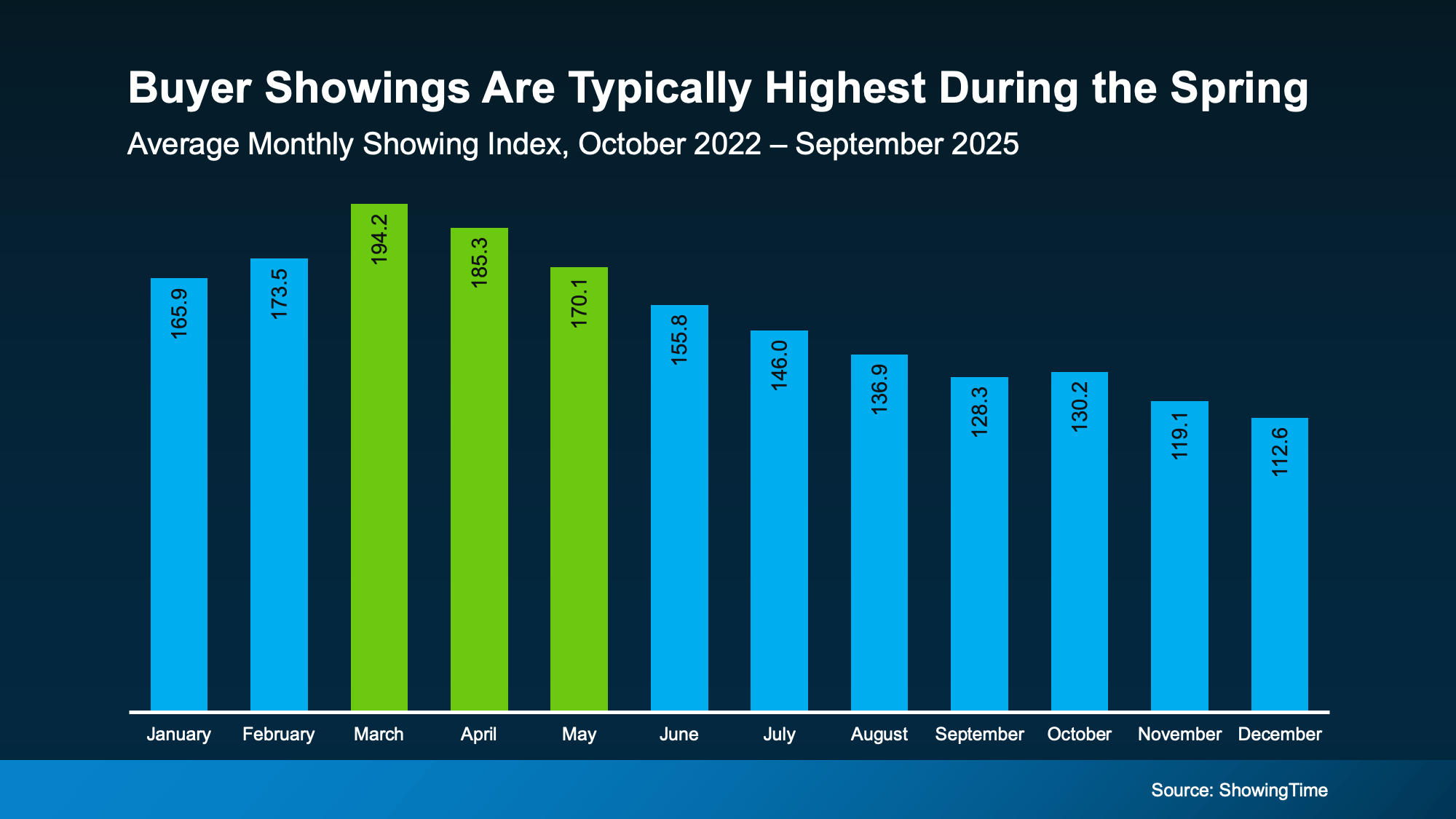

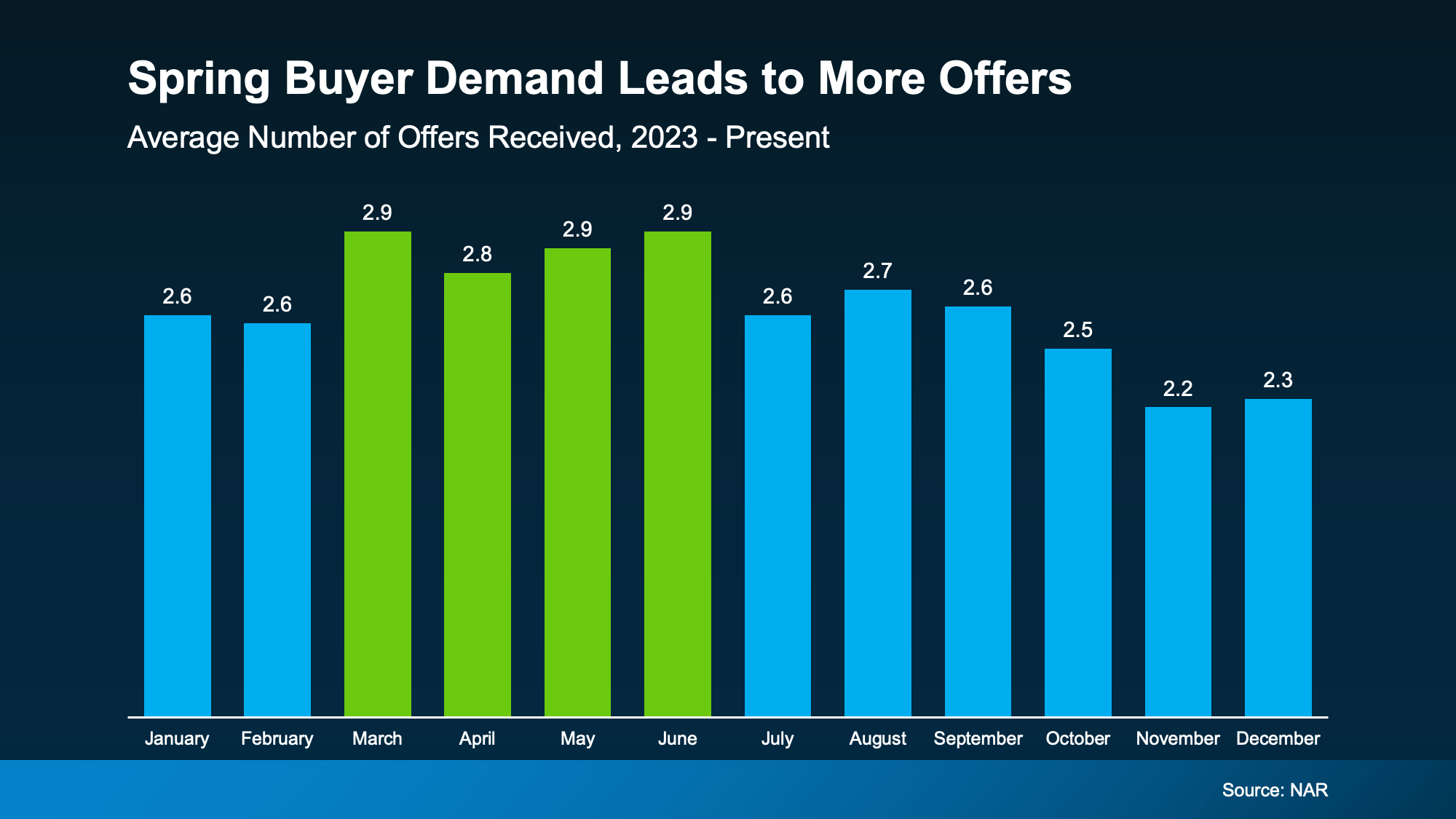

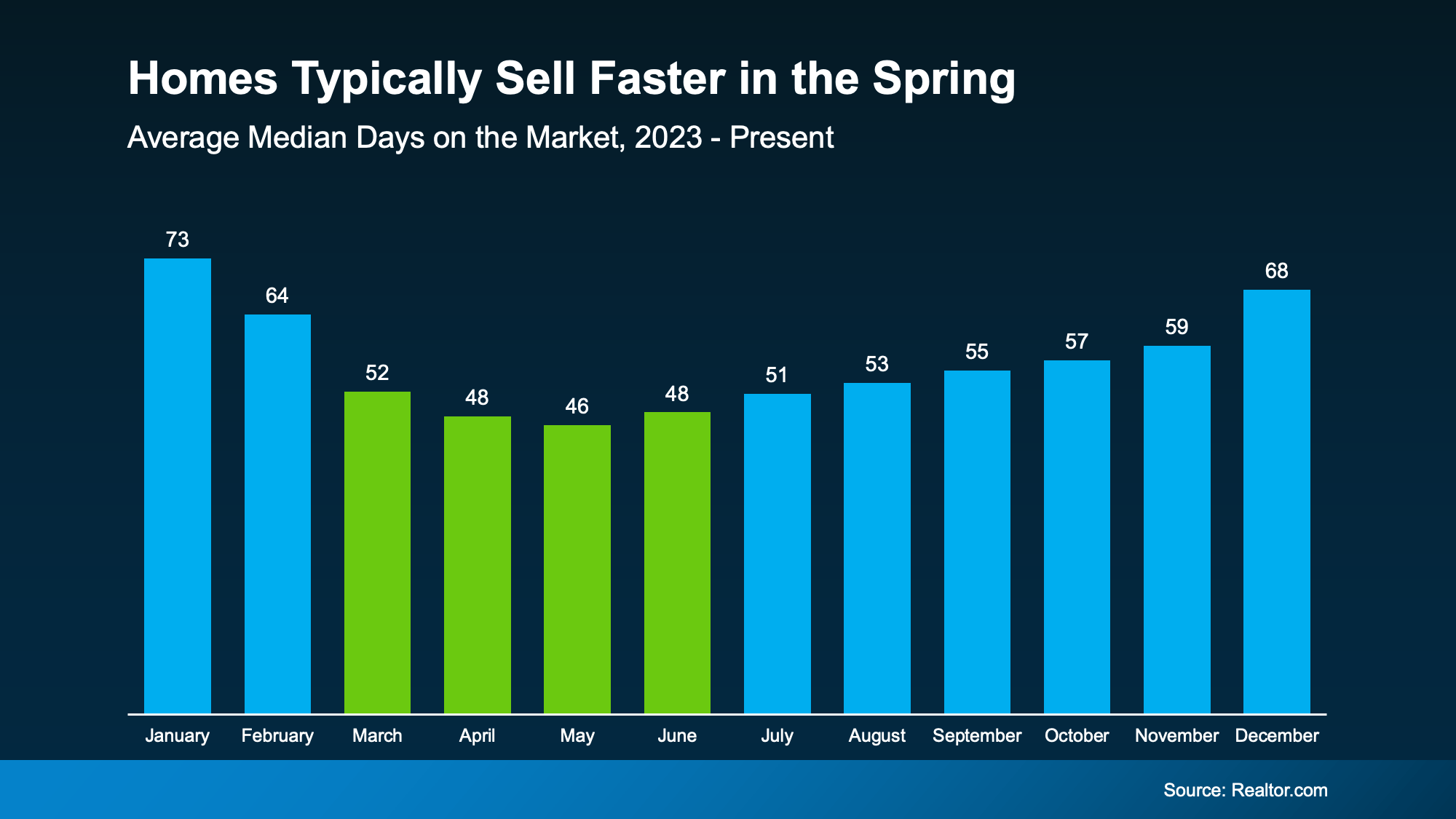

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that’s a difference you can feel.

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that’s a difference you can feel.